If you’ve been putting off solar panels or a home battery because of the upfront cost, the NSW Government just removed your biggest excuse. As of 17 June 2026, eligible households across New South Wales can borrow up to $15,000 at zero interest to install rooftop solar, a battery, and a range of other energy upgrades — and pay it back over ten years.

It’s called the Home Energy Saver program, and it’s a $557 million commitment designed to do one thing: make the upgrades that lower your power bills affordable from day one, instead of years down the track. Here’s everything you need to know, and how it works specifically for solar and battery systems.

What is the NSW Home Energy Saver program?

Home Energy Saver is a NSW Government affordability program that launched on 17 June 2026. It has two parts:

– A zero-interest loan of up to $15,000, available right now, repayable over up to 10 years.

– A cash discount of up to $4,000, coming later in 2026 for lower-income households and concession card holders.

The loan portion alone is a $480 million commitment, and the government expects it to help more than 32,000 NSW households upgrade their homes. The whole idea is simple: energy-efficient upgrades save you money in the long run, but the upfront price tag has locked a lot of families out. Spreading that cost over a decade — with no interest added — changes the maths completely.

How the $15,000 zero-interest loan works

The headline feature is that it’s genuinely interest-free. You pay back exactly what you borrow, and nothing more. On a maximum $15,000 loan spread across ten years, that works out to roughly $1,500 a year, or about $125 a month — with zero interest at any point.

A few practical details worth knowing:

– The money goes to your installer, not to you. Once your system is installed, the loan funds are paid directly to the approved supplier. This keeps the loan tied to the actual upgrade.

– The loans are run by Brighte and Plenti. These two established finance providers administer the credit and handle the approval process under standard responsible-lending rules.

– You’ll need an approved supplier. Your solar and battery installation has to be carried out by a supplier accredited under the program (using CEC-approved panels, inverters and battery products).

Who is eligible?

To qualify for a Home Energy Saver loan, you need to tick all of these boxes:

– A combined taxable household income of $210,000 or less.

– You’re an Australian citizen or permanent resident.

– You own the property where the upgrade is being installed.

Importantly, both owner-occupiers and landlords are eligible for the loan, so investment-property owners can use it too. A NatHERS home energy assessment is optional, not required.

There are a few exclusions to be aware of: you can’t access a loan if the property has already received $15,000 in upgrades under a previous Home Energy Saver loan, or if it’s social/community housing or used for short-stay accommodation.

What can you use the loan for?

While the program covers a long list of upgrades, the two that deliver the biggest, fastest savings are the ones we focus on at Opera Solar:

– Rooftop solar panels — generate your own electricity and slash your daytime grid use.

– Home battery storage — store your solar power and use it at night, when grid prices are highest.

The loan can also be used for EV chargers, switchboard upgrades, solar water heaters, heat pump hot water, induction cooktops, DC ceiling fans, reverse-cycle air conditioning, ceiling insulation, draught-proofing and double glazing. For most households, though, a solar-and-battery combination is where the real bill reduction happens.

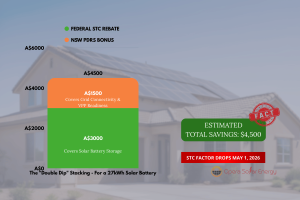

The big win: stack it with the federal battery rebate

Here’s the part a lot of people miss. The Home Energy Saver loan can be combined with the federal Cheaper Home Batteries Program, which already cuts the upfront cost of a typical home battery by around 30%.

The sequence matters: you apply any available discounts or rebates first, then use the zero-interest loan to cover whatever’s left.

A quick worked example. Say you’re installing a solar-and-battery system priced at $15,000:

1. The federal battery rebate reduces the upfront cost of the battery portion by roughly 30%.

2. Your solar panels are already discounted at the point of sale through federal STCs (small-scale technology certificates).

3. You then use a Home Energy Saver loan to finance the remaining net amount — interest-free, over ten years.

The result: a quality solar and battery system with little to no money out of pocket on day one, paid off in small monthly instalments that are often offset by the savings on your power bill.

What about the $4,000 discount?

Alongside the loan, a separate discount of up to $4,000 will open later in 2026. This one is means-tested more tightly — it’s for households with a combined income of up to $80,000, or eligible concession card holders. Renters can also access the discount, as long as they have their landlord’s permission to carry out the upgrade.

If you qualify for both, the advice is to claim the discount first, then take out a loan to cover the rest.

Why now is a smart time to go solar and add a battery in Sydney

NSW has already embraced home energy upgrades in a big way — more than one in two houses in the state now has rooftop solar, and around 13,000 new batteries are being installed every single month. There’s a reason the uptake is accelerating:

– Lower power bills, permanently. Generating and storing your own energy insulates you from rising grid prices.

– Blackout protection. A battery keeps essential circuits running when the grid goes down.

– Energy independence. Use more of what you generate instead of selling it back cheaply and buying it back expensively at night.

– Year-round comfort. Power your heating and cooling from the sun rather than the grid.

With the upfront cost barrier now removed by an interest-free loan, the question shifts from “can I afford it?” to “why wait?”

How to apply for the Home Energy Saver loan

The process is straightforward:

1. Choose an approved installer and decide on your solar and/or battery system.

2. Get a quote so you know the exact amount you need to finance.

3. Apply for the loan through Brighte or Plenti (your installer can guide you through this).

4. Get installed, and the loan funds are paid to your installer on completion.

5. Repay over up to 10 years — interest-free.

You can find full program details and check your eligibility on the official NSW Government page: energy.nsw.gov.au/home-energy-saver

How Opera Solar Energy can help

At Opera Solar Energy, we design and install CEC-approved solar panel and battery systems for homes and businesses across Sydney and regional NSW. We work with both Plenti and Brighte finance(*lending criteria applies, and subject to finance companies approval), so we can help you understand your options and structure your solar-and-battery upgrade to make the most of the Home Energy Saver loan alongside the federal battery rebate.

If you’ve been waiting for the right moment to go solar or add a battery, this is it. Get your free, no-obligation quote today or call us on 1300 271 430, and we’ll help you work out exactly how much you can save.

Frequently Asked Questions about Home Energy Saver Loan

1. Is the NSW Home Energy Saver loan really interest-free?

Yes. It’s a genuine zero-interest loan — you repay only what you borrow, with no interest added at any stage, over a term of up to ten years.

2. How much can I borrow?

Eligible households can borrow up to $15,000. On the maximum amount over ten years, repayments work out to roughly $125 per month.

3. Can I use it for both solar panels and a battery?

Yes. Rooftop solar and home battery storage are both eligible upgrades, and a combined system is one of the most popular ways to use the loan.

4. Can I combine the loan with the federal battery rebate?

Yes. The loan can be stacked on top of the federal Cheaper Home Batteries Program. You apply the rebate/discount first, then use the loan to finance the remaining balance.

5. Do I have to own my home?

For the loan, yes — you must own the property. Both owner-occupiers and landlords are eligible. The separate $4,000 discount (opening later in 2026) will also be available to renters with their landlord’s permission.

6. What’s the income limit?

Your combined taxable household income must be $210,000 or less to qualify for the loan.

7. Who provides the finance?

The loans are administered by two finance providers, Brighte and Plenti, under standard responsible-lending rules.

8. When did the program start?

The loan component launched on 17 June 2026 and is available now. The $4,000 discount component is expected to open later in 2026.